Telcos successfully embedded within Healthcare remain a rare breed. All the more noteworthy then is BT’s virtual ward & care launch in the UK, spanning AI and digital therapeutics, underpinned by two years’ collaborative preparatory work.

Over that period, we’ve had hints on its Healthcare go-to-market intentions, but have had to wait to see how the promised new strategic direction would scope out.

‘Jobs to be done’ will dominate the NHS 2023/24 radar: Clear outcomes; RoI; More of what has supported successful delivery. Tech to underpin weak foundations, boost efficiency, empower.

A tall order, given the new regional Integrated Care Systems (ICS) cluster model is still bedding down. But post pandemic, buyers better appreciate their tech assets. They have a greater awareness of the futility of point solutions, and need for aligned tech and digital investment.

The North Star aspirations don’t disappear, but are de-escalated in the face of more frontline mission critical needs. They’ll also face competition for available budget. The strongest demand potential will come from so-called ‘Arms Length Bodies’ (ALBs) such as the new NHS Transformation Directorate (the merger of NHS England, NHS Digital, and Health Education England), given their remit on national-level futureproofing. However, growth opportunities may be confined to vendor relationships forged through the pandemic.

An NHS Digital Maturity Framework Remains Elusive For Now

If you’re a vendor of US origin, you will likely have been reassured by the partnership between HIMSS and NHS England to co-design a digital maturity assessment framework – recognised internationally, HIMSS provides a solid benchmark on which to pursue and measure excellence. It also helps providers (aka Trusts) to align their investments.

That partnership has been dissolved, with consultancy McKinsey recently awarded a 2-3 year contract to deliver a baseline and an enhanced assessment of maturity across NHS providers and ICSs. Seven pillars will underpin: ‘well-led; smart foundations; safe practice; support people; empower citizens; improve care; and healthy populations’.

NHS England has made several attempts at such an assessment in recent years, yet has achieved very little to-date.

Clearly no-one can wait until this latest project takes off. Common sense alone indicates that maturity levels across ICSs still vary considerably, and will do so beyond 2023. While ambitious and well-led providers have always mapped out their own trajectory, and had the funds to support this, 2023/24 is all about coming together as a local geographic ICS cluster, to audit, streamline, and map immediate priorities.

That of course doesn’t mean that these ambitious providers will stall their strategy while others play catch up. This is an ongoing tension that ICS leaders and their Boards will have to manage.

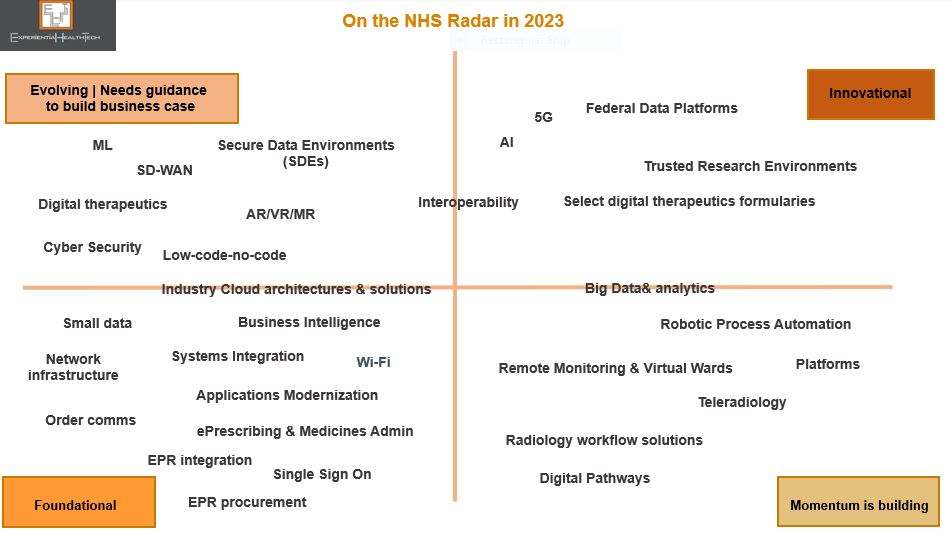

One Provider’s Innovation is Another’s Foundation

To support vendors on where to direct their effort through 2023/24, Experiential HealthTech has mapped out which digital and technology areas are high priority, and therefore most likely to attract available budget.

These priorities are grouped across four categories, to reflect both the disparity in maturity levels at individual provider level, and the greater need to align capability and ambition at ICS level. The technologies listed below are not exhaustive. We are not implying that tech procurement teams will move in linear fashion from one category to another.

This selection also chimes with those frontline operational targets we believe to be of highest collective priority in 2023: earlier diagnosis, referrals, co-ordinated pathways, patient flow, remote monitoring, and workforce management.

Foundational: Providers at this level are largely playing catch up. Note that dozens have yet to deploy an EHR. Amongst those that do have one, order comms modules may not necessarily be in scope. A lack of modern Wi-Fi infrastructure clearly stalls new OOH models of care and inhibits patient-centric services. Cloud may or may not be deployed – the most likely exposure will be through EHR vendors. Even instances of small data may be alien to many clinical and admin teams at this level;

Momentum is building: Providers making investment decisions at this level have already taken successful steps towards more co-ordinated care, and are looking to replicate early wins, to perhaps address co-morbidity. In these contexts, workflow and patient flow are being prioritised. Recognised gains also include richer data collection at a clinical and operational level;

Evolving | Needs guidance to build business case: More mature providers are looking to align and advance their ambition through deployment of these technologies. They may either be aware of peer success in these domains, or feel these to be a next natural transformative step. Either way, they’ve reached the stage where they need support on relevant metrics to include to present their case to the C-Suite;

Innovational: Those individual providers or ICS clusters poised to take evolutionary steps towards more of an ecosystem model, where interoperability is understood, data maturity comparatively high, R&D relationships a part of their remit, and more widely shared governance is culturally appreciated.

The opportunity for you lies in deciding which part of the maturity spectrum you want to support. Each category above offers scope for elasticity on which tech is deployed, so ground your value proposition. Be specific. Meet their goals. Ditch generic promises. Your ability to adapt is key.

At an ICS cluster level, expectation and need converges in relation to data & literacy, cloud, cyber, automation, and integration. User and IT team experiences so far have been mixed, partly through some vendor hype, so step up support for more granular roles-based education, transparent pricing advice, modernization, and workload migration.

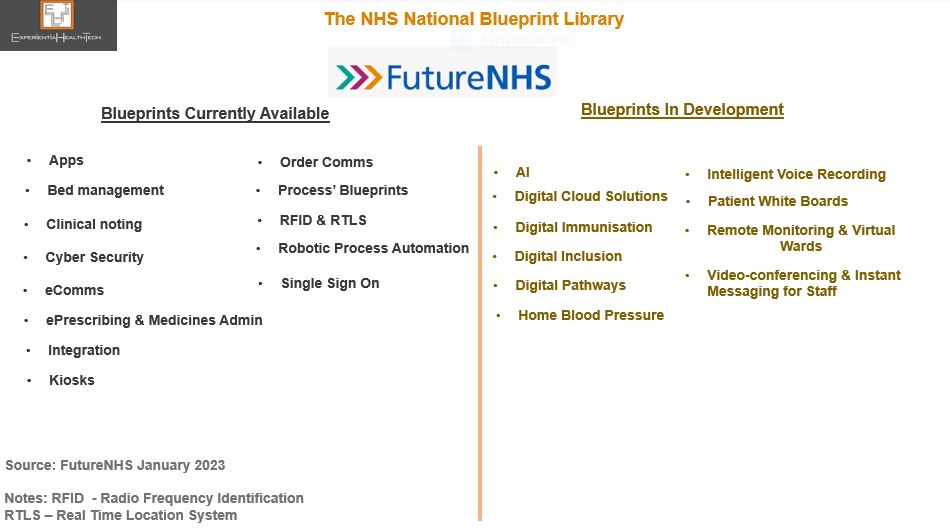

Also worth bearing in mind is the growing peer-to-peer influence via the NHS Blueprints (managed by FutureNHS). Published by providers that have successfully modernised and transformed, they are granular best practice guides. Not all of these blueprints are glamorous, but they clearly illustrate the power of peer influence and gap in transformation and modernisation that’s still out there.

More ambitious tech deployment guides are in the pipeline (see below). Aim to tie in your poster clients here, in context.

One important point to note at this stage is that ICSs are not yet empowered to buy tech and digital as a single buying unit.

Acute care remains the most lucrative demand path, in terms of direct spend, its role as clinical lead on new service models, or partnerships with Life Sciences. Mental health and community less so. Private providers will extend their remit to reduce the NHS frontline backlog, but digital maturity varies greatly here too. GPs are in flux. Social care has yet to line up.

Note that the time to impact buying decisions is shorter this 2023/24 Financial Year, since we have the certainty of a general election by year-end 2024 latest. This mandates a Purdah period, banning new spend from when the election date is announced, until the elected government is in place. That can eliminate six months of activity.

Vendor-Side Jobs to be Done

This ‘sleeves rolled up’ approach applies equally to you the vendor community. Competition continues to intensify, but that doesn’t necessarily reflect a sell-side completely aligned to real world demand.

Incumbents, especially within the clinical software side, continue to add more bells and whistles as a competitive response, without addressing the many enforced workarounds needed to overcome current solutions failings.

Use your current internal cost cutting measures to trigger a reset of priorities, with your partners in tow. Be realistic.

Your pre-sales teams should expect to have to graft harder to qualify leads. Account Managers will need to dig deeper on core and aligned need.

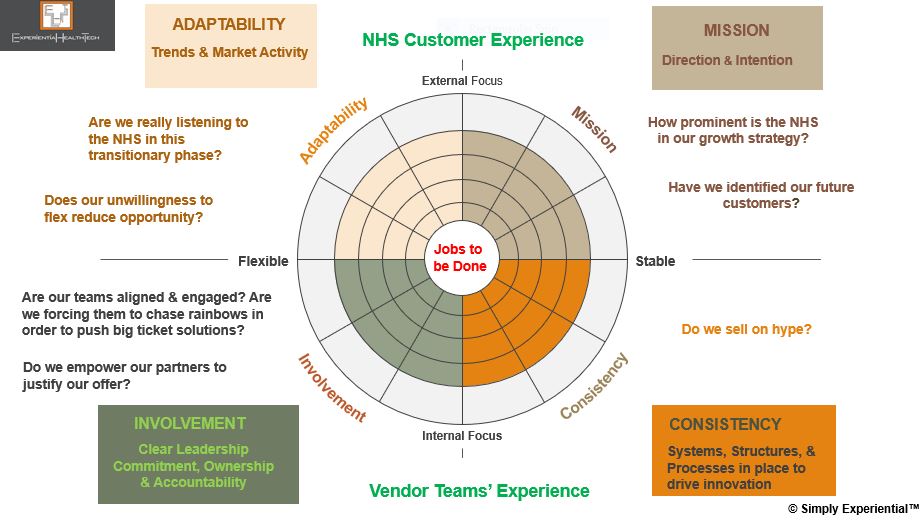

Simply Experiential™ | A Framework for Vendorsand Their Partners

Below are the first-tier components of the Simply Experiential™ framework, which I use with my clients to review the impact of their internal operations on their market success today, as well as their robustness for future-mapping.

It’s a really useful way to bring often disparate teams together, to touch base, strategize, and plan together more effectively.

Your teams and partners explore their beliefs and assumptions about your culture, intention, and context in the market, and assess the spectrum of your capability now and in the future.

While health tech buyers certainly value culture, their loyalty is gained more through a deep-seated commitment to understanding their need at a granular level. Bear in mind that while the vendor and SME community believe they already show this, many experiences shared from across the NHS provider community reveal disconnect, disappointment, and hollow promises.

The framework has more detailed layers, and offers the ability to either hone-in on a specific area that needs to be addressed, or use it to baseline your next steps considerations. Think of it as an anchor to your strategic backbone.

The Bottom Line

The NHS will remain a tough sell in 2023/24. Not all wish lists will be fulfilled. But the tide is turning. With an upcoming general election, it’s natural to anticipate yet further government-led reorganization, especially should a new party get elected into power.

Should the ICS model not survive in name post-2024, its mission will – the NHS has come too far. It’s the many iterations and redesigns over the last decade that have brought the NHS in England to this point. Shaky as it may seem, it’s the best strategic steer we’ve seen, and continues to hold promise.

Effort committed now across your teams will lay down the marker for a greater dividend in the mid-term opportunity pipeline.

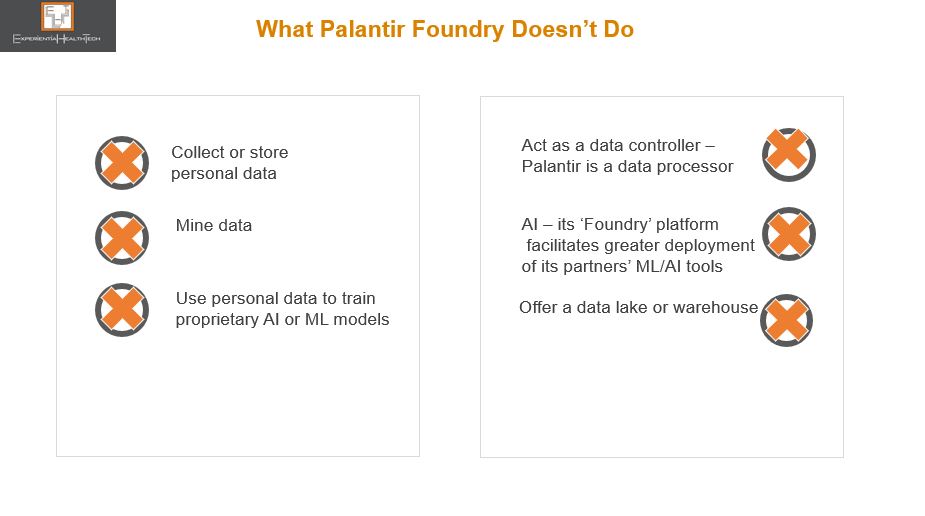

Palantir positions itself as a data harmonizer, integrator, and analytics facilitator, yet its National Health Service (NHS) detractors label it a data thief. The current barrage of recycled criticism surrounding the company is short sighted, when really, Palantir is being scapegoated for a decade of poor NHS leadership on nurturing a data driven culture.

Now, the NHS Transformation Directorate (a merger between the former NHS Digital, NHSX, and NHS England) is spending inordinate amounts of time defending its decision to exploit the effective partnership it forged with Palantir through the pandemic.

One upcoming ‘open’ contract, yet to be run, must rank among the most controversial in the history of NHS technology procurement:

A five-year relationship (with an option to extend by a further 2 years) worth £360m, to co-create a national data analytics platform, aka Federated Data Platform (FDP). This will enable analysis of disparate data streams from across the 42 newly established local Integrated Care Systems (ICSs).

Three key issues underpin the hotly debated and at times mis-interpreted discourse:

Outward behaviour has had the rumour mill running at an all time high that Palantir and NHS leaders have already jointly decided the structure and running of the FDP, so that the open tender is no more than a rubber-stamping exercise, to camouflage the award of the biggest chunk to Palantir. This also includes the recruitment of two former NHS England executives who had been working closely with Palantir through the pandemic;

No NHS-wide debate has been held to champion this next chapter, or reassure frontline teams on data sharing and privacy-by-design. Contrary to general perception, we’re told that the FDP is not intended to directly support patients’ care. It will reportedly initially be used for the national management of vaccines and immunisation programmes, population health, elective waiting lists, and meds & equipment supply chains;

Yet, relationships are further strained when we’re to believe that shared care records, which the vast majority of ICSs now have created in some form, will feed into the FDP. Not everything adds up, and key stakeholders rightly expect transparency;

The company’s heritage in classified security and military-related contracts.

So much so that the release of the tender has been delayed twice so far.

Blinkered NHS Leadership

Perhaps part of the problem here lies in the drive by NHS leaders to accelerate at scale and pace. They have a legacy of spectacular failure in public, patient-advocacy, GP, and provider engagement over data sharing, ownership, and privacy.

That US providers continue to renew Palantir contracts seems to offer no reassurance on issues such as trust and data privacy. If anything, this further stokes the debate on the higher likelihood of the English model ‘descending’ towards privatised healthcare – in a culture steeped in free at the point of care, any mention of patients paying for at least some of their healthcare sparks outright fury. And yet the reality is that the self-payment model has been gaining traction among those unwilling to sit out delays of several years before being offered intervention.

There is a huge spectrum of digitally enabled transformation across the NHS. The successful stories emanate from strong local leadership teams. This in itself represents another oddity within NHS policy here : When it suits, frontline leaders are offered match funding for tech innovation and advised that ‘local knows best”; in other instances, such as with this FDP, a top down model is all but imposed.

Drowning in Data Yet Low Population Health Insight

We know that the ICSs and their aligned Boards have multiple challenges ahead to ensure on par digital maturity, while still grappling with paper-based settings and EPR deficits (a mandate has recently been set to close this deficit).

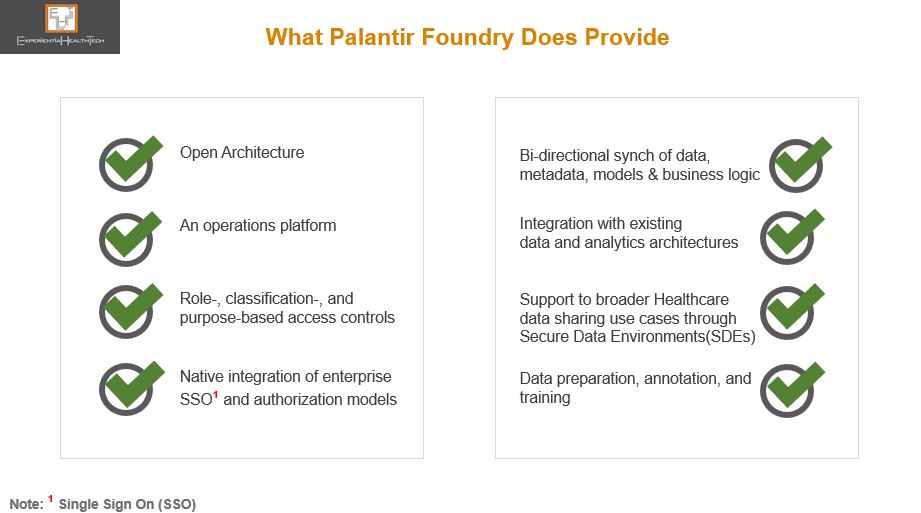

The NHS needs and wants much of what Palantir has to offer: a federated setting with strong governance foundations, interoperability, model-agnostic methods, open architecture, operational & decision intelligence, AI-on-the-fly, AI for IoT and Edge, “co-create once and repurpose”, and vertical platforms.

Most recently, through The London Medical Imaging & AI Centre for Value Based Healthcare, NHS leaders had a golden opportunity to create a wider coalition of the willing among frontline teams, to embrace a federated learning model. That hasn’t happened, with the result that this apparent leapfrog into a longer term and more consequential relationship is drawing such criticism and alarm.

But there is a clear line between both these projects: in the Value Based Care initiative, although tech companies were clearly involved, NHS Digital was in the driving seat. In this FDP initiative, the feeling is that these same leaders are handing over the crown jewels of NHS rich data to Palantir.

The justification for the tender is that the skills needed to build and manage such a platform go way beyond the collective capability of the NHS frontline, at a time of its greatest operational challenge.

While there are clinical and IT leaders who support this move, the drive to embed this nationally is still facing strong resistance. Not to over-simplify the tensions here, it’s worth busting some myths over Palantir:

Palantir Takes Up Mentoring

Palantir has clearly worked its successful pandemic relationship with the NHS to good effect. That approach too has been criticised. But let’s face it, this is no different a tactic from other vendors over the years, including many of those that stood up solutions for free through COVID-19. Equally, many vendors have over the years sought my advice on which among the NHS England/NHS Digital/ NHSX leaders they should woo, to embed their respective tech philosophy.

Palantir has also stepped in to reassure on what to expect, should it win the largest part of the FDP work. But much of the language used is elusive to many frontline teams.

The NHS Transformation Directorate may plough on and coronate Palantir, offering the 3 other related FDP tender parts to other bidders – note that the names in the running are not mainstream to the NHS. One of these vendors has confirmed its intention to submit a bid as part of a consortium.

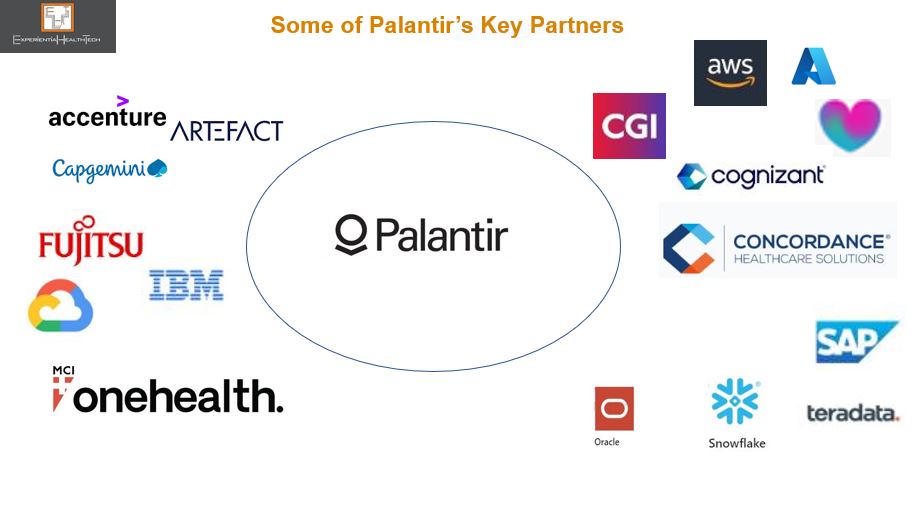

This is a further irony given the range of high calibre partners signing up to work with Palantir in general, many of which independently have forged solid trusted relationships with the NHS, and which within the context of this FDP contract will have to engage with Palantir on some level.

Or, as is currently politically fashionable, we may yet see a U-turn (expensive).

There is perhaps never an optimal time to go ‘big and bold’, but this is what’s being prioritised. This is high stakes for both the NHS and Palantir.

Expect the debate to rage on, post-contract award. This expenditure carries all round high expectation on deliverables and frontline outcomes over the timelines carved out.

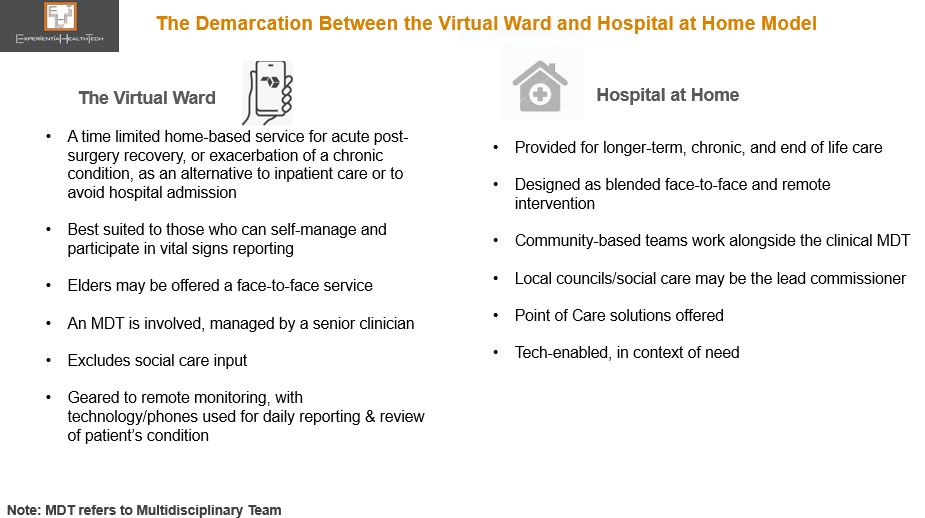

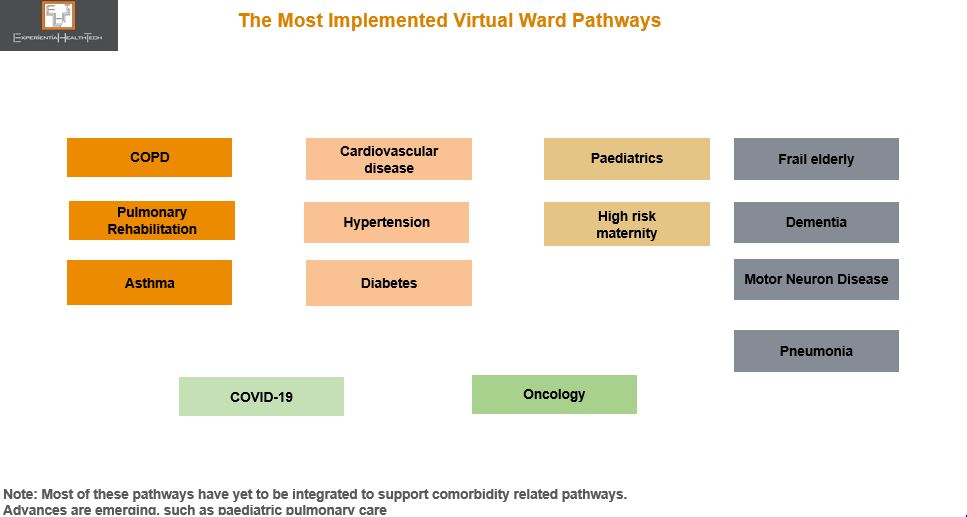

Virtual wards seem a win:win. But some stakeholders are sounding a cautionary note over their sustainability, highlighting the ambiguity about what actually defines a ward. We need to unpick the fundamentals before considering what’s next.

Hailed as a mission critical enabler through Covid, virtual wards, although not new, are being positioned as the common sense answer to many of Healthcare’s service delivery problems. Aligned to ‘RPM’, they offer a clearer context from both the patient and clinician’s perspective, and help frame the service expectation.

But the evidence gathered in support to-date is narrowly confined, relating largely to:

• Earlier discharge of selected patients to continue acute rehab/treatment at home – the emphasis and related costing focusses on releasing hospital beds;

• Wards set up on the fly to deal with covid diagnosed patients – understandably perhaps, cost benefits analysis may be absent.

While the more personalised care elements of the ward are attractive, this promise of on par hospital-grade care is interdependent on a robust back end, even before we consider technology. This is as much about patient-and work flow, and outcomes, as it is bed management. And in the overall backdrop of what most Healthcare systems are grappling with, the messaging risks appearing over-simplistic, downplaying the need to pre-plan heavily.

Care From Anywhere?

Post-pandemic, there’s a clear push to anchor this model. NHS England for example wants its 42 Integrated Care Systems (ICSs) to each plan for between 40 to 50 virtual beds per 100,000 population. Indications from the frontline are that this target won’t be met.

Nonetheless there are NHS success stories, with several providers extending pilots. In July 2022, the Leicester, Leicestershire and Rutland ICS signed Spirit Health, which over time, will implement virtual wards for 16 digital pathways, supporting over one million people.

This is one of the few providers not to position around beds. Plus, it will advance into more complex conditions.

And this reflects the cross roads we‘re at. Virtual wards are critical, but scale-out needs long term aligned local planning, as well as legacy resource and tech issues to be resolved. Wards can’t happen at the side-lines.

Once embedded, they can help underpin the more complex Hospital at Home model. Ireland for example, building towards a tech-enabled reconfigured system, will pursue this route, incrementally building evidence and co-designing with patients from the outset.

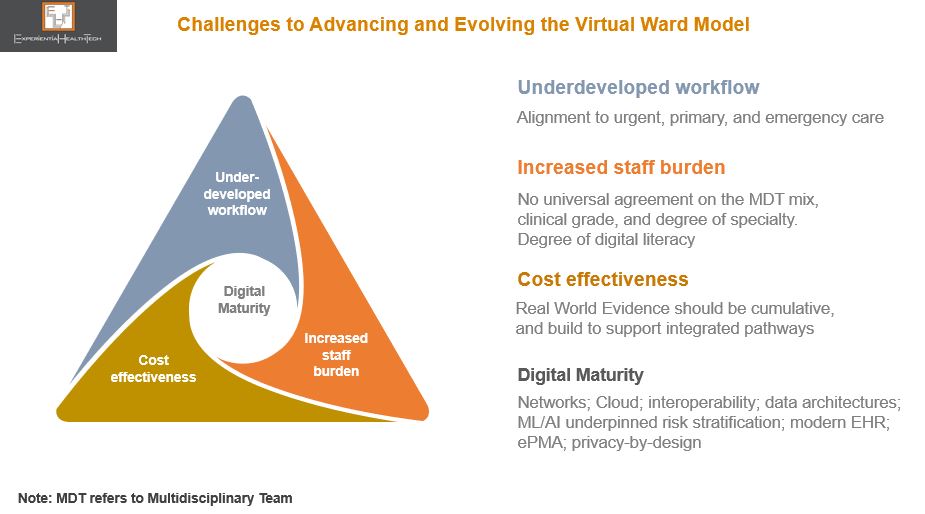

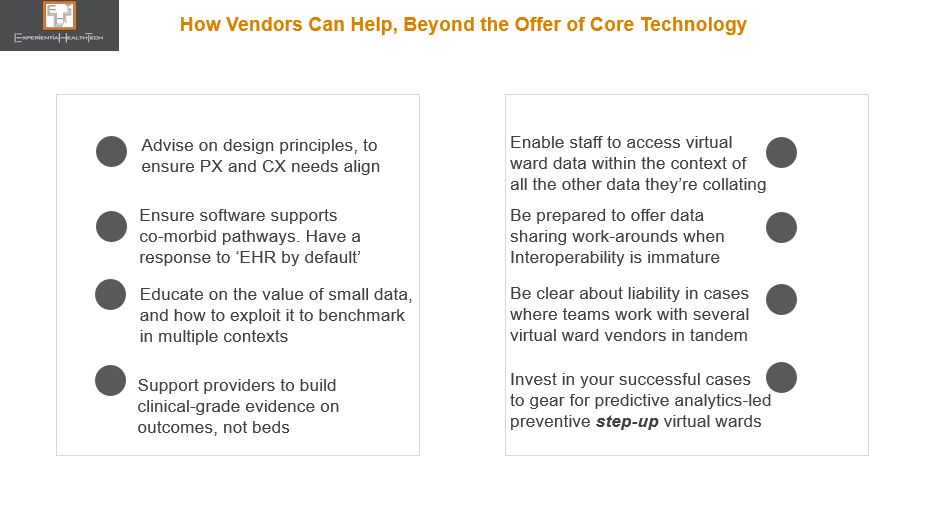

The Open Competitive Field is Intensifying

As more providers look to work through post-pandemic backlogs, there is a golden opportunity to win their trust through lower risk pilot studies – which remain the preferred route – but the race to build share is intensifying.

This is about change management. As the competitive field opens up, more vendors are stepping up to support the virtual ward’s evolution outside their core offer, as a way of differentiating. Support addresses governance, digital literacy, virtual ward champions, Allied Health Provider empowerment, UX, patient education, and data planning.

Some vendors are highly credited in other contexts, and through acquisition see this as a natural portfolio extension. Others also offer at-home nursing, tele-health and prescription delivery services. Some are specialist medtechs, while others offer vital signs monitoring equipment, adaptable to a wide range of pathways.

Some are further differentiating through proprietary technology, but operate within Cloud infrastructures. Partnerships are increasingly key, with the likes of Verizon, Atos, and Medeanalytics being signed.

Virtual wards are about so much more than offering a patient kit, or wearables, and vendors should expect to be tested on several fronts.

Those vendors emerging with freshly minted contracts to either scale across a region or across multiple pathways have used co-design to evidence how a templated approach can accelerate the pace at which multiple other virtual ward pathways are implemented, once the foundations are in place. They are setting the expectation for others to match, or surpass.

Virtual wards are exciting, but they must be handled carefully. And as they evolve, we foresee a defined role for newer players such as Pharma to add value.

Below are some suggestions on how vendors can position on value.

Despite several ‘big story’ headlines over the last few weeks, slamming both the enterprise and health tech sectors for their arrogance in thinking they can crack Healthcare simply, providers do appreciate the value in working with the vendor community.

Equally positively, as more advance along their Transformational and digital journey, they now recognise the need to shift from a transactional to a collaborative relationship: that they too have a role to play to ensure a tech partnership is successful; that they must better articulate their needs.

The just-published review, “Better, Broader, Safer” relates specifically the NHS and its technology and HLS partners, but it’s equally applicable to every other entity across the data ecosystem that wants a working or commercial relationship with the NHS – the start-up community, telcos, social care, and private healthcare. In one way or another, all these relationships are bound by a need to share existing data and generate new data and forge insight.

Many of the widely respected author Ben Goldacre’s recommendations are already (independently) being applied in pockets of Europe and the US.

Sustaining Our Communities Through Networked Wellbeing Villages

It’s a bold promise to offer personalised, preventive, integrated healthcare & wellbeing within a socially cohesive community. The Welsh regenerative project, Pentre Awel, aims to deliver.

Unlike projects such as Saudi Arabia’s NEOM City, this is tailored to supporting the local community’s needs- high deprivation, unemployment, an ageing population, and chronic co-morbidity. Geared to be high-tech and high-touch, participatory care, shared facilities, and telemedicine will be standard.

Age UK’s report on the impact of prolonged self-isolation on elders reveals deteriorating health and increased medication. The outcome? Escalating polypharmacy and medication errors. Northern Ireland is pioneering in response.

With the value of real-time data access so evident during this pandemic, the conversation on AI has become amplified X-fold across healthcare systems, Research, and Pharma (‘Healthcare’). Great news for many among you. But you can make an even deeper contribution by committing to the drive for ethics.

Ethics relates to how, in the absence of any framework, all stakeholders can work to set clear parameters on the safe adoption and integration of AI – to build towards consistency across real-world settings (clinical and in the community), discovery research, and smart city design.

No-one is suggesting that tech solutions have been sold on hype. But since regulators are deemed to not yet have all of the appropriate skills to evaluate good AI, Healthcare is taking ownership, to scrutinise validity and tech impact across the AI life cycle.

Is a UK Next Gen Private Healthcare Model Taking Shape?

Any mention of private healthcare in the UK tends to provoke. But patient-driven demand for private intervention has been steadily growing year-on-year, creating a new segment – the self-payer.